Market Update week ending 9 February 2024 – POSITIVE US EMPLOYMENT DATA WHILST CHINA RALLIES AND OIL PROVIDES OPPORTUNITIES

![]()

POSITIVE US EMPLOYMENT DATA WHILST CHINA RALLIES AND OIL PROVIDES OPPORTUNITIES

This week the headline news has been the continued decline of government bonds. The drop was sparked by a really positive US jobs report which showed more than 350,000 new jobs were created in January. This was far higher than expected and, combined with above inflation wage growth, adds potential upward pressure for inflation. Central bankers have also been pushing back against the idea of early rate cuts and rising activity in services sectors in the US and UK added weight to their arguments.

The Chinese government stemmed the decline of equity markets. A mix of regulatory action and direct intervention helped Chinese indices stage a recovery. The timing of the intervention is convenient. Markets are now closed for a week as the country celebrates Lunar New Year and the government will hoping that the break will allow some of the negative sentiment to dissipate. It also gives the government extra time to come up with a more permanent way of restoring confidence. But the fact this intervention was needed remains a concern for investors.

Meanwhile, Brent Crude continues to bounce around between US$74 per barrel and US£83 per barrel following Angola leaving the oil producers organisation OPEC over a dispute on output quotas. It followed the recent decision by the 13 member cartel and 10 allied nations of OPEC to slash oil production in 2024 to prop up volatile global prices which hasn’t been helped by the Gaza conflict and shipping being attacked in the Red Sea.

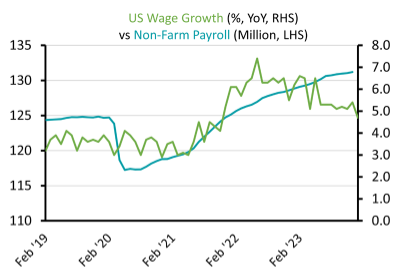

![]() US : EQUITIES MAKE GAINS BUT BONDS SUFFER

US : EQUITIES MAKE GAINS BUT BONDS SUFFER

Positive news lifted tech stocks as the broad US equity market made further gains. Chip designer Arm said artificial intelligence presents a profound opportunity for its business as it reported robust sales and lifted its profits forecast. Shares in Uber increased as declared its first annual profit and Spotify reported a 23% increase in subscribers. The big tech stocks also made further gains to drive the wider market higher.

However, government bonds fell in value as the US jobs market proved resilient. More than 350,000 new jobs were created in January after similarly strong hiring in December. US wage growth was also higher than expected. Officials from the Federal Reserve and Bank of England repeated warnings that interest rates will not be cut as early as some investors expect. This pushed down government bond values and pushed yields up. Meanwhile, the OECD forecast that the global economy will slow slightly this year and expects inflation will fall more slowly as it warned any surprise increase will spark volatility in markets..

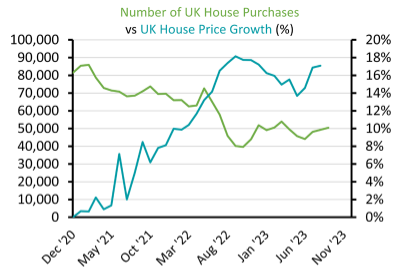

UK : OUTLOOK FOR HOUSING IMPROVES

UK : OUTLOOK FOR HOUSING IMPROVES

The UK is expected to have fallen into recession in the final quarter of 2023. GDP fell by 0.1% in the third quarter of 2023 and The National Institute of Economic and Social Research expects to see GDP contract for the second successive quarter when official figures are released next week. Meanwhile consumer spending continues to slow. Sales in January increased 1.4% compared to last year, but this is lower than the 1.9% increase in December and the value of retail sales has been below inflation for some time. The Recruitment and Employment Federation said hiring has slowed and starting salaries have fallen below the long-term average.

Not all news this week was gloomy as the UK’s services sector continues to expand and the outlook for the housing market has improved. The number of mortgage borrowers has increased as borrowing rates fall. Estate agents report more buyers and sales and the monthly surveys from Nationwide and Halifax show average house prices are rising.

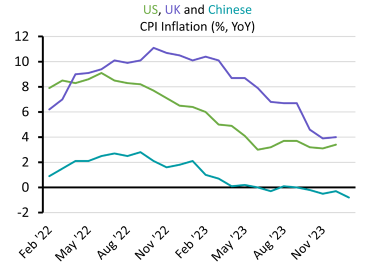

CHINA : EQUITIES RALLY BUT DEFLATION REMAINS A CHALLENGE

CHINA : EQUITIES RALLY BUT DEFLATION REMAINS A CHALLENGE

Chinese equities increased significantly following further government intervention. In addition to more restrictions on short selling, there was a big increase in trading volumes this week as state-controlled entities combined to buy equities on Chinese exchanges. The head of the financial regulator was also sacked as the government tried to reassure investors. The big Chinese stock market indices increased by between 3.5% and 5% this week in advance of a week-long closure for the Chinese new year holiday.

Meanwhile, Chinese deflation is getting worse. Consumer prices have been falling since October and CPI came in at -0.8% in January, down from -0.3% in December. Deflation is a greater problem for producer prices. The annual rate of producer price index is -2.5% and prices have been falling since October 2022. Falling prices in China are likely to help disinflation in developed economies. They also increase the chance of monetary stimulus from the Chinese central bank, which added to the positive sentiment towards equities.

![]() COMMODITIES: OIL PRICE TRADING RANGE OPPORTUNITIES

COMMODITIES: OIL PRICE TRADING RANGE OPPORTUNITIES

The effect of the Gaza conflict and the resultant attacks on shipping in the Red Sea, and OPEC slashing oil production has been that Brent Crude has for the moment settled into a fairly predictable trading range, with US$74 per barrel being low end and US$84 per barrel being it’s upper end. This has provided us with a fairly predictable trading range, which we have been able to take advantage of for our clients. Over the past 7 days we are just under +7.0% up, which we will taking the profits from imminently. Since the Gaza conflict we have had 3 successful very short-term trades in oil which, together with the latest success has produced a combined net after fees profit of around +12.0%. We are always mindful that oil prices can be volatile and so we went several months without investing prior to the latest 3 trades, which we felt confident were predictable enough in terms of settled trading range to be able to profit without very much risk for those clients who provided their authority to do so.

(* note: clients whose funds are invested via offshore bonds, investments into commodities such as oil and gold are not permitted).

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset Management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.

Yours sincerely,

Phil Simmonds

Philip A. Simmonds MBA, LL.B(Hons), FPFS, Chartered MCSI

Chartered Wealth Manager | Chartered Financial Planner

Solicitor-Advocate (company in-house solicitor)

E : phil.simmonds@private-office.co.uk

phil.simmonds@private-office.law (for legal matters)

This document has been prepared for general information only and is not guaranteed to be complete or accurate. It does not

contain all of the information which an investor may require in order to make an investment decision. If you are unsure whether

this is a suitable investment you should speak to your financial adviser. You may get back less than you originally invested.

Private Office Asset Management is authorised and regulated by the Financial Conduct Authority