Market Update week ending 28 July 2023

![]()

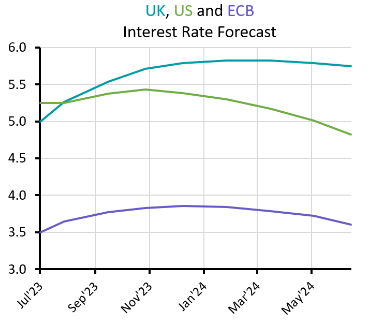

US FEDERAL RESERVE & ECB DELIVER EXPECTED RATE HIKES

This week there were no particular surprises as the Federal Reserve and European Central Bank (ECB) delivered rate hikes as they were expected to do. By stating that rate decisions will be determined by the data, the outcome of these meetings was effectively settled some weeks ago. The more interesting subject is where rates go from here. There has been speculation about whether this is the end of the road for rate hikes in the US and Europe, or there is more to come. However, the strong US GDP numbers and cooling EU data means this remains a live issue. US treasury yields were unmoved by Wednesday’s decision but climbed after the GDP numbers yesterday.

Only a few months ago, the ECB was widely seen as having further to go to tame inflation but cooling European economies means markets now expect US and European rates to peak at roughly the same point. Next week it is the turn of the Bank of England. Markets still see the UK as the outlier and are predicting rates will soon overtake the US and peak at a higher level. Sticking to the data-driven narrative gives central bankers room to manoeuvre if the environment changes. But this also allows room for markets to be caught out if surprising data demands a response.

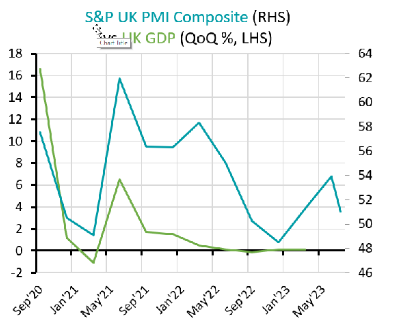

UK : COMPANIES DEFY GLOOMY OUTLOOK FOR NOW

UK : COMPANIES DEFY GLOOMY OUTLOOK FOR NOW

Despite the pessimism surrounding the UK, a wide range of companies have delivered positive trading updates. Centrica has reaped the benefit of recent sky-high gas prices as it reported half-year profits have risen by almost 10 times to £969m. Shares in Rolls Royce surged after it said its turnaround plan is working well and it continues to benefit from the resumption of air travel following Covid.

Companies including BT, Moneysupermarket, Lloyds, Barclays, GlaxoSmithKline, Unilever, Reckitt Benckiser, Foxtons and Frasers Group all reported revenue and profits above forecast. Rising rates have raised bank profits, while the rising cost of living has increased the use of comparison websites. Rising London rents means revenues from Foxton’s rental division have offset the drop in sales. Even companies without favourable trading conditions are beating expectations. Frasers (the owner of Sports Direct and Evans Cycles) reported annual profits are up 40% as younger consumers are happy to pay for premium brands.

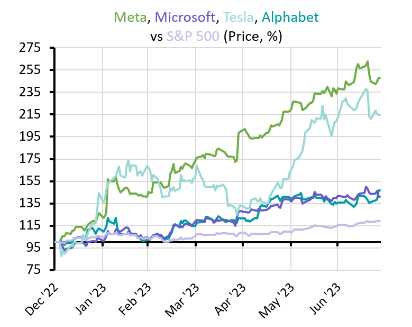

![]() US : TECH STOCKS CONTINUE TO OUTPERFORM

US : TECH STOCKS CONTINUE TO OUTPERFORM

US equities have remained bullish as the quarterly reporting season progresses. The big seven tech companies of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla now account for around 30% of the S&P 500. These stocks have risen between 41% and 211% so far this year and are responsible for most of the gains for US equities in the recent rally. As a result, there is a lot a riding on their continued strength.

Four of the seven companies have issued updates so far. Tesla’s shares fell last week as it announced further price cuts to boost market share. Microsoft exceeded its forecast, however, recent enthusiasm for artificial intelligence meant markets were disappointed with its reported growth. But Alphabet saw its shares rise as it reported better than expected advertising revenue and Meta’s shares surged after it said revenue in the second quarter increased by more than 11%. These gains have helped US equities rise again this week. Apple and Amazon are due to report next week and Nvidia’s update is due at the end of August.

![]() GLOBAL : BANKS STICKING TO THE SCRIPT

GLOBAL : BANKS STICKING TO THE SCRIPT

As stated above, the Federal Reserve and ECB both delivered a 0.25% interest rate hike in line with expectations. The increase from the US Fed followed its decision to hold rates last month, but strong employment and retail spending plus sticky core inflation meant this week’s additional hike was no surprise. The ECB is slightly behind the Fed in its hiking cycle and it was also widely tipped for another hike as employment also remains very strong in the EU. The lack of surprises meant markets remained very calm, with US and European bond yields almost unchanged.

Attention will now turn towards the next interest rate meetings. Federal Reserve chair Jerome Powell has left the door open for further rate hikes without appearing to favour any further action and said the outcome would depend on economic data. The ECB also appeared slightly less aggressive as it communicated its decision and markets are looking at this week’s hikes as the potential end of the current hiking cycle.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset Management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.