Market Update week ending 28 April 2023

CALL FOR WAGE RESTRAINT BADLY RECEIVED

Last week Bank of England chief economist, Huw Pill, caused some controversy when he said that to break the inflationary spiral people in the UK need to just accept they are poorer and stop pushing for wage increases. This may be a sensible suggestion to an economic problem, but people see the falling purchasing power of their earnings and rising mortgage costs as more than a rational exercise in economic theory. The strong stock market updates from consumer-facing firms show those with strong brands have been able to protect their profits by passing on price hikes in full, pushing up inflation. This has been good news for investors, but when consumers think they are the only ones being asked to shoulder the burden of rising prices, the argument put forward by Pill was never going to be well received.

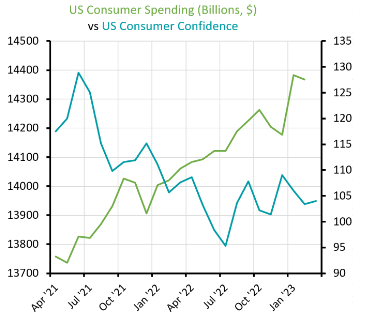

Meanwhile, despite weak consumer confidence, a slowing US economy was propped up by robust consumer spending. Service activity has grown strongly in developed economies but headwinds from rising interest rates and tighter bank lending will further test consumer resilience.

![]() US : TECH STOCKS LIFT US EQUITIES

US : TECH STOCKS LIFT US EQUITIES

Rising interest rates and disappointing sales weighed on technology stocks in 2022 but reports from the first quarter show tech companies returning to growth. Microsoft and Google-owner Alphabet said earnings were above forecast, as they reported rising revenues from their cloud computing divisions. Meta Platforms, owner of Facebook, also reported a return to growth as advertising revenues were better than expected. All three tipped developments in AI as central to future growth. US tech stocks have outperformed the broader US market this year and positive updates this week have given technology stocks a further leg up.

It was not all good news for Microsoft as its plans to expand its gaming business suffered a setback. Its $75bn acquisition of Activision Blizzard was blocked by the Competition and Markets Authority, which said it would stifle competition in the growing online gaming market. Shares in Activision fell around 10% but are still up on the pre-offer price.

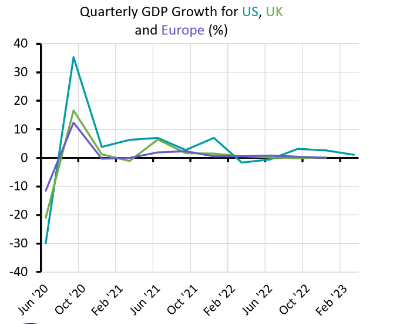

![]() GLOBAL : STRONG SERVICES ACTIVITY PROPS UP WEAK ECONOMIC GROWTH

GLOBAL : STRONG SERVICES ACTIVITY PROPS UP WEAK ECONOMIC GROWTH

US GDP growth slowed sharply in the first quarter of the year, despite other indicators showing economic activity remains relatively robust. GDP increased by 1.1% in the three months to the end of March, when compared with a year earlier. This is considerably below the 2.6% recorded for the last quarter of 2022 and well below many forecasts. Despite slowing growth, initial unemployment claims were lower than expected as the jobs market remains strong. EU GDP for Q1 came in as expected at 1.3%.

Other recent updates are more positive for growth. Business activity has increased rapidly in the US, UK, Japan and Eurozone according to the latest figures from S&P Global. Initial Purchasing Managers’ Indices show economic output for the UK, US and EU in April increased at the fastest rate since last May. For most regions this is being driven by a big increase in services, as manufacturing output declined everywhere except the US. However, consumer confidence in most developed markets remains weak.

![]() US : PRICE INFLATION BOOSTS BRAND PROFITS

US : PRICE INFLATION BOOSTS BRAND PROFITS

Consumer businesses with strong brands are continuing to benefit from the ability to pass on rising costs to their customers. Despite rising wages and input costs, companies including Coca-Cola, PepsiCo, Procter & Gamble, Unilever and Nestle all declared higher profits in the first quarter as they passed on above inflation increases to consumers. Unilever increased prices by an average of 11% last quarter, PepsiCo increased prices by 16%, while Nestle increased prices around 10%. High food costs have been one of the biggest contributors to elevated CPI inflation in recent months.

This year total consumer spending in monetary terms has risen, although not as fast as inflation, but many regions have seen sales volumes decline as shoppers feel the effect of rising prices. Companies with the strongest brands have been able to buck this trend and have experienced little or no drop in sales volumes, despite rising prices. This trend has helped the MSCI Quality index to outperform the MSCI World index this year.

![]() PRIVATE OFFICE ASSET MANAGEMENT – NEWS

PRIVATE OFFICE ASSET MANAGEMENT – NEWS

Sebastian Simmonds BSc. (Hons), ACSI

Director | Investment Portfolio Manager & Financial Planner

We are delighted to congratulate Sebastian on his 2 recent qualifications having completed his Level 4 Investment Advise diploma and his Level 4 Certificate in Financial Planning & Advice. To complete matters he also recently achieved the CISI exam “Integrity Matters”. Sebastian will now be signed off as competent as an FCA Authorised Client Adviser and with this he gained his well-earned and significant promotion this month to “Investment Portfolio Manager & Financial Planner”, and is now entitled to use the CISI designatory letters ACSI.

Sebastian has been with the firm for more than 7 years, including his time as a work experience during his A-Levels, and then as a full time trainee after he completed his degree in Business Management (Entrepreneurship) with Business Experience in June 2019. Sebastian became a Director of the firm in 2022, and has become a very capable, reliable and integral member of the firm.

Well done Sebastian!

In the meantime, Imogen continues at pace with completing her LL.M Masters Degree in law, and also her Post Graduate diploma in Legal Practice, following completion of which she will be admitted to Roll of Solicitors in England Wales. Imogen will then begin her Investment Advise diploma, whilst she continues in her role as Business Development Manager with us.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset management and should not be construed as advice.