Market Update week ending 24 November 2023 – CONSUMER CONFIDENCE IMPROVING?

CONSUMER CONFIDENCE IMPROVING?

This week the outlook for the UK and the US rests in part on consumer confidence and how that might translate to spending which will ultimately result in economic growth. Although confidence appears to have unexpectedly improved in the UK, there is another energy price cap increase hike coming in January 2024. Meanwhile, US consumer confidence has weakened slightly and some of the data points to a slowdown in retail spending. US markets were positive in advance of the Thanksgiving holiday and investors will be looking at whether this positivity carries through to the annual retail spending bonanza that is Black Friday.

Meanwhile, in the UK, the Chancellor Jeremy Hunt attempted to improve disillusioned voters by reducing National Insurance Contributions (NICs) for employees and the self-employed (but not the 13.8% employers’ rate of NICs). The early introduction of this cut in January, rather than the new tax year on 6th April 2024, has caused speculation about the possibility of a Spring election in 2024 rather than the autumn as the Conservatives weigh up whether this is long enough for workers to feel the benefit, against the potential for a rate hike if inflation returns. The Office for Budget Responsibility (OBR) assessment of the outlook was lukewarm at best. It expects low growth this year and next, but says inflation will take until the second quarter of 2025 to return to target.

UK : CHANCELLOR TARGETS ECONOMIC GROWTH

UK : CHANCELLOR TARGETS ECONOMIC GROWTH

Chancellor Jeremy Hunt used an improved outlook to announce the cut to National Insurance in advance of a general election campaign next year. The OBR predicts the UK will avoid recession with GDP growth of 0.6% in 2023 and 0.7% in 2024. However, it expects inflation will not return to the target 2% until 2025. In addition, the ability for businesses to offset 100% of capital investment in the first year has been made permanent as part of 110 reforms designed to support business growth. Other measures include reform of infrastructure planning and boosting foreign investment which the Treasury hopes will increase business investment by £20bn a year by 2033.

The autumn statement has forecast lower government borrowing as a more resilient economy increased tax revenue. The OBR also expects annual borrowing to fall from 4.5% of GDP this year to 3% next year. However, the drop in future borrowing was not a great as investors expected and bonds fell following the speech, driving bond yields up.

![]() US : MARKETS IN POSITIVE MOOD

US : MARKETS IN POSITIVE MOOD

Members of the US Federal Reserve presented a united front on its recent decision to leave interest rates unchanged. Minutes from the last meeting show the bank’s voting members warning of the need for rates to remain high enough to restrict economic activity and saying the bank needs to proceed carefully to allow time for recent rate hikes to have an effect. Other central bankers including European Central Bank (ECB) President Christine Lagarde and Bank of England governor Andrew Bailey have also warned against prematurely declaring victory in the fight against inflation. The balancing act of increasing rates to arrest inflation but not too high to avoid a recession is a difficult one.

A sharp decline in US durable goods orders caused US Treasury bonds to rise at the start of the week as investors took this as a sign of economic slowdown, despite a decline in new unemployment claims. There was a small decline in US consumer confidence ahead of the key holiday shopping weekend which starts with Black Friday. However, US equity markets were in positive mood as technology and consumer discretionary sectors led a broad gain.

![]() GLOBAL : OIL PRICE FALLS, BUT OUR RECENT OIL TRADE NETS OUR CLIENTS +2.89% AFTER TRADING FEES

GLOBAL : OIL PRICE FALLS, BUT OUR RECENT OIL TRADE NETS OUR CLIENTS +2.89% AFTER TRADING FEES

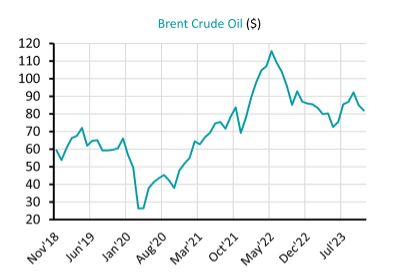

The global oil price fell 5% on Wednesday amid signs of tension between OPEC member states as the organisation seeks further production cuts to support the oil price. Brent Crude has fallen around 13% from a peak of $93 a barrel in September to $81 last week and at the beginning of this week it has fallen a further -1.53% to $79. The decline has been put down to a number of causes. These include lower demand as global economic growth cools combined with higher inventory levels in the US. Supply from non-OPEC members such Iran has also been increasing this year.

Saudi Arabia has driven this year’s production cuts and recently confirmed it’s production cap will be in place until at least January 2024. However, disagreement over how to share any additional production cuts led to speculation that Saudi may abandon its production limit. The oil price has since regained the losses and it is up slightly this week. The lower price of oil has helped ease global inflation this year and fears that the outbreak of war between Israel and Hamas and the ongoing war in Ukraine would push up oil prices have so far failed to materialise despite an early spike at the beginning of the conflict in Gaza.

Despite the fall in the price of oil last week, we cashed out to a zero holding and netted +2.89% profit for our clients in 5 days, having traded in on 16th November at $77.42, and we continue to monitor the moving trading range of Brent Crude looking for that bargain strike price.

![]() PRIVATE OFFICE ASSET MANAGEMENT – KEEPING VOLATILITY LOW HAS BEEN THE KEY TO OUT-PERFORMANCE

PRIVATE OFFICE ASSET MANAGEMENT – KEEPING VOLATILITY LOW HAS BEEN THE KEY TO OUT-PERFORMANCE

As we enter December this week, we can reflect on 2023 as being a very challenging year for investors! It is very easy to lose sight of the recent good times during periods of difficulty, and so it is useful to just recap on the 18 months we enjoyed prior to the more recent and well documented global economic challenges.

- From 1st June 2020 to November 2021 our Balanced Risk clients enjoyed net growth of more than +16% on average.

- The 7iM Balanced Risk Multi-Asset Benchmark was up +5.6% over the period thus we out-performed the benchmark by more than +10%

- Due to the most cautious assets being hardest hit during the period, the Cautious Risk Benchmark was down -1.8% over the period

- We out-performed the Cautious Benchmark by around +18.0%.

- The FTSE-Gilts All Stocks Index fell by -8.9% during that period, so having avoided Gilts, we out-performed that traditionally cautious asset class for our clients by circa +25% over the period.

To put matters into perspective, from November 2021 to November 2022, whilst our Balanced Risk client portfolios were down circa -5.0% over the 12 month period we still managed to out-perform the multi-asset benchmarks by +6.3% against benchmark performance of -11.8%, with the major indices suffering significant losses between November 2021 to November 2022 as follows:

- FTSE100 -4.07%

- FTSE250 lost -24.06%

- German DAX lost -16.7%

- Pan European EUROSTOXX50 lost -15.60%

- US Tech Market NASDAQ lost -30.01%

- US S&P500 lost -19.47%

- FTSE Gilts ALL Stocks Index lost -18.32%

From November 2022 to the current round of Rebalancing Proposals, we are around level, with continued out-performance of the multi-asset benchmarks.

There are two major considerations when advising on and managing funds:

- Performance (of course – that’s the bit that interests our clients because that’s what they see and that’s what matters!)

- Volatility. Volatility is the measure of risk held within a client’s portfolio across the time-weighted aggregated assets held throughout a period of time. To us at private Office Asset Management it is absolutely a key objective to carry as little ‘real risk’ as possible during challenging global economic climates where we are seeing bank failures, outbreaks of war, high inflation, significant interest rate hikes and potential recessionary impact.

We take preservation of our clients capital very seriously indeed, and we are delighted that we have been able to keep volatility significantly lower than the benchmark during these challenging times, as demonstrated in our performance data accompanying the current ReBalacning Preoposals. This has meant that we have needed to be more active than usual, but our higher trading activity has certainly paid off. As we look to enter 2024 in just over 1 month, we expect the level of trading to reduce as we hopefully return more to normal.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset Management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.

Yours sincerely,

Phil Simmonds

Philip A. Simmonds MBA, LL.B(Hons), FPFS, Chartered MCSI

Chartered Wealth Manager | Chartered Financial Planner

Solicitor-Advocate (company in-house solicitor)

Chief Investment Officer