Market Update week ending 22 March 2024 – MARKETS RISE ON HOPES OF SPRING RATE CUTS

MARKETS RISE ON HOPES OF SPRING RATE CUTS

This week falling inflation and positive updates from central banks helped generate an optimistic mood. Equities have done well so far this year, but bonds have struggled due to the tension between central banks and markets’ assumptions about rate cuts. Investors have been forced to readjust as inflation remained sticky and central banks appeared reluctant to move too early. However, positive inflation updates and signs that jobs markets are cooling, plus signs that apparently insatiable US consumer demand is slowing have caused a big shift in central bank messaging.

Members of the ECB have been noticeably more upbeat about rate cuts, while Bank of England governor Andrew Bailey talked of the need to be forward looking, and said inflation doesn’t need to be back to target before acting. In the US, Jerome Powell was similarly optimistic about progress on inflation and investors and central banks appear to be settling on late spring as the date for the first rate cuts. There is still plenty of scope for disappointment but markets are enjoying the outbreak of positivity as bonds have been able to join the rally.

![]()

US & UK : RATES HELD FOR NOW

US & UK : RATES HELD FOR NOW

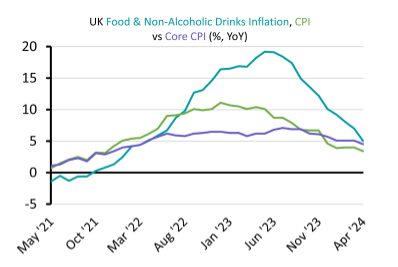

The Federal Reserve and Bank of England left interest rates on hold. The decisions were in line with expectations but markets have been encouraged by positive messages from the central banks. The Fed raised its forecast for economic growth to 2.1% for this year and the consensus among voting members is for interest rates to be reduced by 0.75% to 4.75%. Bank of England governor Andrew Bailey said slowing inflation means things are moving in the right direction to allow rate cuts. UK headline inflation fell from 4% in January to 3.4% in February, mainly due to falling food prices.

EUROZONE : RATES ALSO HELD

EUROZONE : RATES ALSO HELD

The European Central Bank also appears to be adopting a less aggressive approach to interest rates. With inflation in Europe continuing to fall back towards target, members of the ECB suggested the first rate cut in the Eurozone could be as early as June and that markets may expect several rate cuts this year. Government bonds have rallied this week, sending yields down, and US equities have led global markets higher.

JAPAN : DIFFERENT INFLATION ISSUES

JAPAN : DIFFERENT INFLATION ISSUES

The Bank of Japan increased interest rates for the first time since 2007. The rate hike brings the era of negative central bank interest rates to an end as inflation appears to have settle around 2% after years of no or negative inflation. The small rate hike takes the BoJ interest rate to a range of 0% to 0.1% and the bank also formally ended its programme of buying Japanese government bonds. The rate hike helped Japanese equities climb around 6% this week and the yield on Japanese government bonds increased.

Meanwhile, the Swiss National Bank surprised markets by cutting rates as it reduced its main interest rate from 1.75% to 1.5%. The Swiss experience of inflation has been very different to the rest of western Europe. Inflation peaked at 3.5%, far below the Eurozone, and it dropped to 1.2% in February allowing the SNB to cut rates to help make the Swiss franc more competitive and boost economic growth, which is forecast for 1% this year.

RETAIL : CONSUMER DEMAND COOLING

RETAIL : CONSUMER DEMAND COOLING

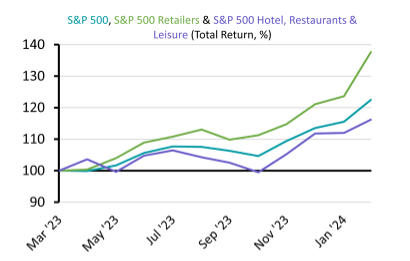

After three years of very strong consumer demand, many US retail businesses are reporting a slowdown in sales. A number of reasons have been given for the slowdown, including consumers finally exhausting the excess saving built up during Covid restrictions. Retailers also say some reluctance to spend is due to rising economic uncertainty and a cooling jobs market. The rapid rise of interest rates means the average US household now spends as much paying back personal borrowing as they do repaying mortgage loans. Delinquency rates have also climbed sharply.

Retail sales increased in February but annual growth continues to slow. Value retailer Dollar Tree is planning to close 1,000 stores as spending by its lowest income customers has fallen significantly. However, it is not just lowest income Americans who are spending less as companies including McDonalds, Pepsico and Expedia say sales growth has slowed, while Kraft Heinz and retailer Target reported a decline in total sales.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset Management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.

Yours sincerely,

Phil Simmonds

Philip A. Simmonds MBA, LL.B(Hons), FPFS, Chartered MCSI

Chartered Wealth Manager | Chartered Financial Planner

Solicitor-Advocate (company in-house solicitor)

E : phil.simmonds@private-office.co.uk

phil.simmonds@private-office.law (for legal matters)

This document has been prepared for general information only and is not guaranteed to be complete or accurate. It does not contain

all of the information which an investor may require in order to make an investment decision. If you are unsure whether this

is a suitable investment you should speak to your financial adviser. You may get back less than you originally invested.

Private Office Asset Management is authorised and regulated by the Financial Conduct Authority