MARKET UPDATE WEEK ENDING 20 OCTOBER 2023 – UK GILTS & US TREASURIES UNDER PRESSURE AGAIN AS OIL AND GOLD SOAR

UK GILTS & US TREASURIES UNDER PRESSURE AGAIN

AS OIL AND GOLD SOAR

This week neatly illustrates the problem facing the central banks. In the case of the Bank of England, for example, inflation remains stubbornly high and wage growth continues at near record levels, but consumer confidence and spending have contracted sharply. It is usually good to treat a single month’s data with a healthy dose of scepticism. However, the monthly CPI reading is now stuck at 6.9% where it has been since July. High interest rates are now having the restrictive effects intended on consumer activity, but inflation seems to have stopped reacting to the downward pressure. The bank’s choice is a stark one between tackling inflation and stifling economic growth.

In the US, the Fed has indicated that it will leave rates on hold at its next rate setting meeting, but US consumption is speeding up rather than slowing and markets have concluded the higher for longer doesn’t rule out another hike later this year. Bond markets have looked at the data and concluded that tackling inflation is, and will remain, the priority of central banks and this has dragged government bonds down again.

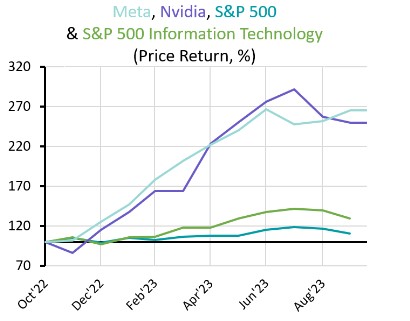

![]() US : US TECH STOCKS FACE SCRUTINY

US : US TECH STOCKS FACE SCRUTINY

US companies have delivered mostly positive stock market updates as the quarterly reporting season picks up pace. The news from Wall Street banks was mixed as profits fell at Goldman Sachs and Morgan Stanley but Bank of America, Citigroup and JP Morgan reported rising profits. Attention now shifts to the largest US tech firms as the gains from US equities this year have been driven by just seven tech firms.

Tesla was the first of the big tech firms to give an update and its shares fell after it reported revenues are down as it concentrates on building market share. It also said delivery of its latest model would be slower than expected. Next week brings updates from Alphabet, Amazon, Microsoft and Facebook-owner Meta Platforms, with Apple reporting the following week. Nvidia has been the standout performer in the S&P 500 this year but its shares fell after the US government announced further restrictions on exports to China. Its next stock market update is expected in mid-November towards the end of earnings season.

CHINA : GDP BOUNCE BACK

CHINA : GDP BOUNCE BACK

The Chinese economy grew by 1.3% in the third quarter as annual growth recovered to 4.9%. This reflects lower activity at this time last year due to the Covid lockdowns, but it also shows government efforts to revive the economy may be taking hold. Business investment increased last quarter partly due to government attempts to develop high-tech manufacturing following the introduction of US export bans on sensitive technology such as the latest microchips. Retail activity also recovered as consumer spending in September was 5.5% higher than in 2022.

However, the Chinese economy still faces a number of serious problems. The property market is stuck in a downturn as prices fall and buyer activity is subdued. Giant developer Country Garden had avoided financial difficulties until this week when it defaulted on a US dollar offshore bond. The strength of the dollar also adds to China’s problems. The yuan has fallen around 10% against the dollar this year and it continued its decline this week.

UK : BONDS SLIDE ON INFLATION CONCERNS

UK : BONDS SLIDE ON INFLATION CONCERNS

UK inflation came in stronger than expected last month. Headline CPI inflation was unchanged at 6.7% as rising petrol and diesel costs and rising prices in some service industries interrupted the recent decline. Average earnings also exceeded expectations as they increased by 7.8% for the year to end of August. However, there are signs the UK employment market is cooling as the number of job vacancies has fallen to 988,000 from a peak of 1.3 million in May. Meanwhile US retail sales were 3.8% higher than 12 months ago, far higher than expected, as strong wage growth supports demand.

Sticky inflation and above inflation earnings growth both increase the chance of a rate hike at the next meeting of the Bank of England. This caused UK government bonds to fall again this week, pushing yields higher. US government bonds have also fallen steeply as the increase in US consumer spending adds to inflationary pressure and makes the US Federal Reserve more inclined to keep interest rates high.

![]() PRIVATE OFFICE ASSET MANAGEMENT – PRESENT CAUTIOUS POSITION PAYING OFF VERSUS THE MARKETS

PRIVATE OFFICE ASSET MANAGEMENT – PRESENT CAUTIOUS POSITION PAYING OFF VERSUS THE MARKETS

The past weeks have been difficult for both the equity and bond markets. Our present positioning across all of our risk rated bespoke managed advisory portfolios has certainly paid off over the past week or so, with our top 3 present aggregated positions across our portfolios currently being as follows:

- Cash – 44%

- Brent Crude Oil – 8.85%

- Physical Gold – 6.16%

Last week Brent Crude rose by +4.14% and Gold rose by +3.98%. Our recent Oil and Gold purchases are currently up, net of fees, +6.05% and +4.18% respectively, and whilst we would prefer not to hold large allocations of cash long term, our ability and willingness to do so as a strategic position versus falling markets has proven to be a very significant to our advisory model compared to the DFM’s who will not / can not hold more than around 5% to 7% max even in plummeting markets. So as regards to the cash holding, we are wating for the risk-asset prices (equities and bonds) to retreat to the levels where they represent very good value and then we will look to purchase them at the lower prices.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset Management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.

Yours sincerely,

Phil Simmonds

Philip A. Simmonds MBA, LL.B(Hons), FPFS, Chartered MCSI

Chartered Wealth Manager | Chartered Financial Planner

Solicitor-Advocate (company in-house solicitor)

Chief Investment Officer

E : phil.simmonds@private-office.co.uk

phil.simmonds@private-office.law (for legal matters)

This document has been prepared for general information only and is not guaranteed to be complete or accurate. It does not

contain all of the information which an investor may require in order to make an investment decision. If you are unsure whether

this is a suitable investment you should speak to your financial adviser. You may get back less than you originally invested.

Private Office Asset Management is authorised and regulated by the Financial Conduct Authority