Market Update week ending 2 June 2023 – US DEBT CEILING DEAL CAN’T HIDE GLOOMY OUTLOOK

![]()

US DEBT CEILING DEAL CAN’T HIDE GLOOMY OUTLOOK

This week the biggest headline was about the deal to prevent the US government defaulting on its debts. When it came to the crunch, Congress and President Biden’s administration managed to achieve the basic function of government by keeping the lights on. However, by suspending the debt ceiling rather than reforming it or scrapping it, the problem is likely to be back after next year’s presidential and congressional elections.

While US markets took a bit of a bump from the conclusion of the deal, over here things are a bit more gloomy. European inflation is falling steadily but shop price inflation in the UK continues to run at a record high rate. Even the sight of food inflation beginning to slow doesn’t offer much to get enthusiastic about yet, as prices are still rising more than 15% a year. Further evidence of the difficulties facing the housing market add to the UK’s headwinds, as borrowing becomes more expensive and falling house prices are likely to depress consumer spending. The gloom is not confined to the UK. China hasn’t managed to defy the global slump in manufacturing so commodity prices have continued their recent slide.

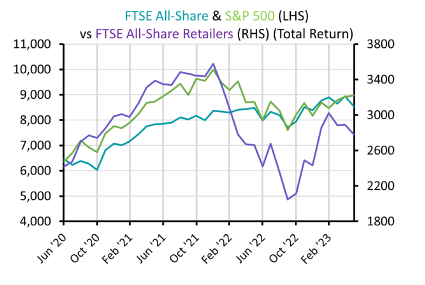

UK : RETAIL PRICE INFLATION REMAINS TOO HIGH

UK : RETAIL PRICE INFLATION REMAINS TOO HIGH

Retail inflation has continued to rise as the UK faces a new warning of recession. The British Retail Consortium said shop prices increased by 9% in May, up from 8.8%. Food prices are still rising fast but have slowed slightly as lower energy and commodity costs begin to filter through. Rising prices have supported listed retailers but this appears to be running out of momentum as retailers report sales volumes are falling. However, the Office for National Statistics (ONS) said retailers and manufacturers are not using inflation to boost profits as average profit margins are in line with the long-term average.

Rising costs have had a negative effect on business confidence as Lloyds Banking Group reported a decline in business sentiment for the first time in three months. Meanwhile house prices are still falling as mortgage rates rise again. Net mortgage lending dropped in April, and the number of approvals also fell. The combination of headwinds prompted ratings agency Moody’s to warn it expects the UK to slide into a mild recession this year.

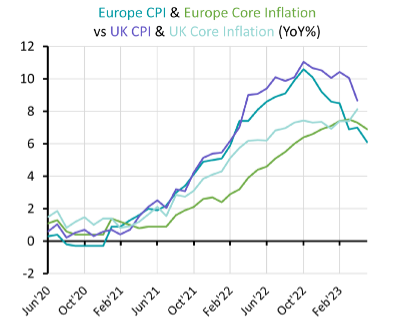

EUROPE : FALLING ENERGY COSTS HELP REDUCE INFLATION

EUROPE : FALLING ENERGY COSTS HELP REDUCE INFLATION

European headline inflation has fallen faster than expected due to lower energy costs. EU headline CPI inflation fell from 7% to 6.1% in May as food inflation also slowed. Core inflation (excluding volatile energy and food costs) fell more than expected as it dropped from 5.6% in April to 5.3%. The EU data was not a particular surprise as several of the continent’s biggest economies including Germany, France and Spain had already reported a slowdown in their inflation rates.

Although consumer confidence remains low, European consumer expectations for inflation are now starting to fall as well. This is in contrast to the UK where rising food costs are only just beginning to slow. European Central Bank president Christine Lagarde was quick to say further rate hikes are still necessary. However, the better inflation data caused speculation that the ECB will hike by 0.25% at this month’s meeting before pausing. German, French and Spanish government bonds have all risen slightly this week.

![]() GLOBAL : WEAKER CHINESE DEMAND WEIGHS ON COMMODITIES

GLOBAL : WEAKER CHINESE DEMAND WEIGHS ON COMMODITIES

Disappointing Chinese economic growth has contributed to falling commodity prices. China’s manufacturing and exports were expected to bounce back following the removal of the country’s strict anti-Covid measures in December. Despite a jump in retail activity economic growth has so far been underwhelming and has contributed to a more muted outlook for global economic growth.

The price of oil has been falling since its peak of $120 last June. Brent Crude is currently around $72 a barrel, and it has dropped around 5% this week due to the latest weak manufacturing output data from China and growing oil stocks in the US. The lack of Chinese demand and the easing of some shortages following Russia’s invasion of Ukraine have been pushing down the prices of a wide range of raw materials. Copper, iron, steel and aluminium are all down between 18% and 30% over the last 12 months and many other industrial commodities have seen their prices fall considerably more.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.