Market Update week ending 16 February 2024 – UK ECONOMY – TECHNICAL RECESSION BUT INFLATION FALLING

UK ECONOMY – TECHNICAL RECESSION BUT INFLATION FALLING

This week we got what should have been monumental news that the UK is officially in recession. The specific definition being used for this head-line isn’t particularly useful however. Most people would associate a recession with rising unemployment, something we have yet to see. So far belt tightening in the retail sector is dragging down growth figures thanks to poor Christmas sales but if it keeps up, we can expect job losses eventually. That the last six months haven’t exactly been great for the UK economy should come as no surprise to anyone.

Elsewhere, the mood is likely more upbeat over at the Bank of England. A recession is the best known cure for inflation and they’ve been trying one cause one ever since they started jacking up interest rates. How bad things need to get and for how long before they’re satisfied will be questions they’ll need to answer. In an election year this could be a boon to Labour who can now blame the government for causing a recession, but there is every chance the figures could be revised up in a few months and the Conservatives will take the credit for a recovery so it’s probably a wash.

![]() GLOBAL : MARKETS CHOPPY AS US AND UK SIGNAL DIFFERENCES

GLOBAL : MARKETS CHOPPY AS US AND UK SIGNAL DIFFERENCES

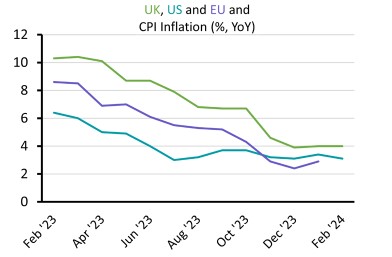

Government bond markets experienced high levels of volatility as contrasting inflation readings in the US and UK cast doubt on the timing of central bank interest rate cuts. Headline consumer inflation in the US dropped from an annual rate of 3.4% to 3.1% but this was higher than expected due to rising costs of housing and services. Monthly CPI and core inflation (excluding more volatile food and energy costs) were also higher than expected. The inflation numbers added to doubts that the Federal Reserve would cut interest rates in the spring and caused government bonds and US equities to fall.

However, contrasting news from the UK helped markets recover as UK inflation was better than expected. Headline CPI inflation was tipped to rise in January but it remained unchanged at 4% as food prices fell for the first time in two years. Core inflation was unchanged at 5.1%. The more positive news helped push UK gilts towards a gain for the week and helped calm US bond and equity markets.

UK ECONOMY : TECHNICAL RECESSION CONFIRMED FOR Q4 2023

UK ECONOMY : TECHNICAL RECESSION CONFIRMED FOR Q4 2023

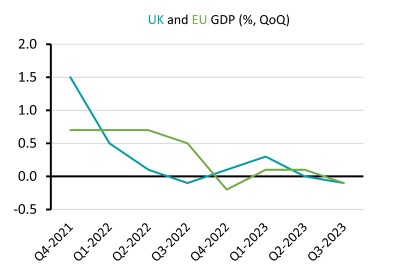

The UK is expected to have fallen into recession in the final quarter of 2023. GDP fell by 0.1% in the third quarter of 2023 and The National Institute of Economic and Social Research expects to see GDP contract for the second successive quarter when official figures are released next week. Meanwhile, consumer spending continues to slow. Sales in January increased 1.4% compared to last year, but this is lower than the 1.9% increase in December and the value of retail sales has been below inflation for some time. The Recruitment and Employment Federation said hiring has slowed and starting salaries have fallen below the long-term average.

Not all news this week was gloomy as the UK’s services sector continues to expand and the outlook for the housing market has improved. The number of mortgage borrowers has increased as borrowing rates fall. Estate agents report more buyers and sales and the monthly surveys from Nationwide and Halifax show average house prices are rising.

UK EQUITIES : CONSUMERS HAVE BECOME MORE CAUTIOUS

Large consumer brands are warning of slowing sales due to a combination of high inflation and low consumer confidence. Heineken said higher prices are starting to affect sales. The world’s second-largest brewer said sales volumes fell 4.7% in 2023 and the company reduced its forecast for profits in 2024. Coca-Cola HBG (the London-listed European bottling company) reported strong profits growth but said it had to make adjustments to its pricing and promotions as consumers have less to spend. Meanwhile Sainsbury’s, JD Sports and Electrolux all say sales of non-essential and big ticket items have been weaker as shoppers choose cheaper alternatives or defer their spending.

UK consumer discretionary stocks have significantly outperformed the broad equity market over the last 12 months as companies such as Next and Unilever have managed to maintain sales volumes or even pass on higher than inflation price hikes. However, this week’s updates show consumers’ ability and willingness to accept further price increases is being tested.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset Management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.

This document has been prepared for general information only and is not guaranteed to be complete or accurate. It does not contain

all of the information which an investor may require in order to make an investment decision. If you are unsure whether this

is a suitable investment you should speak to your financial adviser. You may get back less than you originally invested.

Private Office Asset Management is authorised and regulated by the Financial Conduct Authority