Market Update week ending 15 September 2023 – GLOOMY ECONOMIC DATA POINTS TOWARDS CENTRAL BANKS ENDING RATE HIKES

GLOOMY ECONOMIC DATA POINTS TOWARDS CENTRAL BANKS ENDING RATE HIKES

Last week there were strong signs that we may be entering the final phase of central banks’ battle against inflation. The European Central Bank increased rates for what most many financial analysts believe is the last time, while poor growth data and rising unemployment suggest the Bank of England’s drive to slow the economy and address the tightness in the labour market (bank speak for increasing unemployment) is having the desired effect. In the United States the picture was more mixed. Headline inflation picked up due to rising fuel prices, but underlying inflation figures looked promising.

Elsewhere, the International Energy Agency (IEA) said demand for oil will peak this decade, much earlier than previously forecast, due to the rapid growth of renewable energy generation and electric vehicles (EVs). The sudden pickup in EV sales has catapulted China to the number one spot in vehicle exports as the nation has a clear lead in EV manufacturing because it does not have the burden of large legacy industry to transition. The news spooked Germany to the extent the EU announced an investigation into Chinese manufacturers because they claim Chinese manufacturers are unfairly subsidised.

UK : GDP FALLS BUT WAGES RISING FAST

UK : GDP FALLS BUT WAGES RISING FAST

Economic activity fell sharply in July due to a combination of the unusually wet and cold weather and strike action caused GDP to fall by 0.5%. This is the largest monthly decline since December 2022. The UK jobs market is showing some signs of weakness as the unemployment rate increased 0.5% to 4.3% between March and June. The housing market is also showing more signs of stress as mortgage borrowing fell sharply and the number of mortgages in arrears has jumped to the highest level in seven years.

The poor economic data has fed speculation that the Bank of England will leave interest rates unchanged at next week’s meeting of the Monetary Policy Committee (MPC). This helped UK gilts to rally slightly although sterling continued to fall against the dollar. However, average wages increased by 7.8% during the second quarter of the year. However, this week Catherine Mann, a member of the MPC, said she favours further rate hikes to prevent inflation from crystallising at its current elevated level.

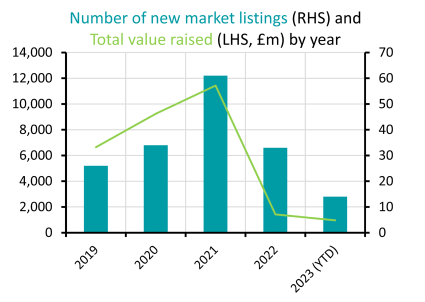

![]() GLOBAL : INVESTOR DEMAND FOR NEW LISTINGS TESTED

GLOBAL : INVESTOR DEMAND FOR NEW LISTINGS TESTED

Shares in UK-based microchip designer Arm started trading in New York. Arm delisted from the London Stock Exchange in 2016 after it was bought by Japanese investment firm Softbank and its return to public markets is seen as a test of investor enthusiasm. The listing was heavily oversubscribed and its shares were priced at $51. The was top of the valuation range and valued the company at $54bn to makes this the largest listing in the US this year.

The last two years have seen a big drop in the number of companies listing on global stock markets but Arm is one of several high profile new IPOs. US online grocery firm Instacart is set to debut on Nasdaq this month with a valuation of around $7.5bn. German sandal maker Birkenstock is also planning to list in the US, with a potential valuation of $8bn. The UK has been a very small number of listings in 2023 but broker Cavendish says it expects to see a noticeable change later this year, particularly for small and mid-sized firms.

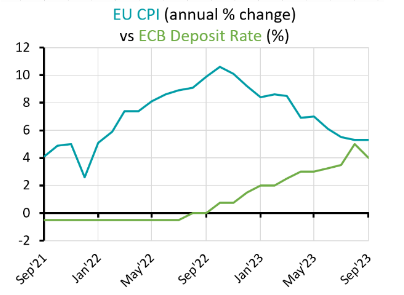

EUROPE : ECB HIKES RATES BY 0.25%

EUROPE : ECB HIKES RATES BY 0.25%

The European Central Bank increased interest rates by 0.25% to take its benchmark rate to an all-time high of 4%. Earlier this week the European Commission reduced its outlook for economic growth from 1% to 0.8% this year and from 1.7% to 1.4% in 2024 and this led to some speculation that the ECB would hold rates at this week’s meeting. Instead, the bank increased for the 10th consecutive time, although it gave a strong hint that rates are now at or very close to their peak. The ECB has updated its forecast for inflation, saying it now expects the headline rate to be between 5.4% to 5.6% by the end of the year and just over 3% by the end of 2024. The euro fell sharply against the US dollar, and European government bonds rallied.

Meanwhile, US government bonds declined slightly after the latest inflation reading came in stronger than expected. Rising petrol prices have pushed up headline inflation from 3.2% to 3.7%. Core inflation (excluding food and fuel) fell again despite housing costs rising fast.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset Management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas

covered this week.

Yours sincerely,

Phil Simmonds

Philip A. Simmonds MBA, LL.B(Hons), FPFS, Chartered MCSI

Chartered Wealth Manager | Chartered Financial Planner

Solicitor-Advocate (company in-house solicitor)

Chief Investment Officer

E : phil.simmonds@private-office.co.uk

phil.simmonds@private-office.law (for legal matters)

This document has been prepared for general information only and is not guaranteed to be complete or accurate. It does not

contain all of the information which an investor may require in order to make an investment decision. If you are unsure whether

this is a suitable investment you should speak to your financial adviser. You may get back less than you originally invested.

Private Office Asset Management is authorised and regulated by the Financial Conduct Authority.