Market Update week ending 14 June 2024 – EUROPE MOVES TO THE RIGHT

![]()

EUROPE MOVES TO THE RIGHT

This week we witnessed significant volatility in European markets after nationalist parties made significant gains in the European parliamentary elections. In France, president Emmanuel Macron called a snap election as he gambles that, when it comes down to it, voters may be less keen to put right-wingers in charge in Paris. With his party already a minority in the National Assembly, Macron is already facing problems passing new legislation and the final calculation is that even if the Rassemblement National (RN) party win, he hopes it could stop Marie Le Pen winning the 2027 presidential election, and he hopes a few years in control of the French parliament may put the French public off the RN for good.

However, the move is fraught with risk for Macron. Early polls show little decline in support for RN and the potential for Macron’s Renaissance party to lose up to half their 250 seats. Macron could also find himself sharing power with a prime minister he shares little with except a mutual loathing. Markets have taken a look at the outcome and decided they dislike both the uncertainty and RN’s programme of unfunded spending.

All this is in stark contrast to what has been happening in the UK, as a large Labour majority is predicted by the pollsters in the upcoming general election, which will move the UK to the left.

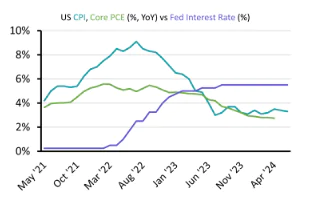

CENTRAL BANKS : Fed holds rate but signals a cut

US inflation fell slightly in April as CPI dropped from 3.4% to 3.3%. Although this is a small decline, markets welcomed the return of disinflation as CPI fell for the second month in a row. Core inflation (excluding changeable food and energy costs) also fell. The drop in CPI helped US government bonds rise slightly early in the week. The Federal Reserve left interest rates unchanged in a decision which was widely expected. But the Fed’s forecast of only one rate cut in 2024 caused US treasuries to give back some of its gains, and helped the dollar remain strong.

The European Central Bank was keen to calm hopes of a rate cut at its next meeting as several members, including president Christine Lagarde, signalled there will be no more cuts before September. European government bonds have had a volatile week, but the potential for the ECB to cut rates more aggressively than the Fed prompted several commentators to say they now see more value in European government bonds than in US treasuries.

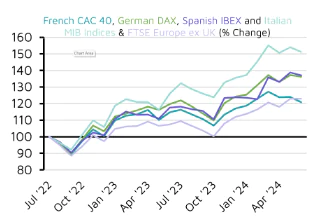

EUROPE : Markets rattled by snap election in France

European financial markets were rocked by the strong performance of right-wing and nationalist parties in the European parliamentary elections. French equities led European markets lower as president Emmanuel Macron called a snap general election after his party came a distant second to the right-wing Rassemblement National (RN) party led by Marine Le Pen. If the RN party wins the election on June 30 then Macron would be forced to share power and appoint a prime minister from Le Pen’s party.

Macron intends to stay on as president until his term ends in 2027, regardless of the result of the general election. However, the uncertainty caused by the election caused the French CAC 40 index to fall more than 3.5% and led other major European indices lower. Banking stocks were particularly hard hit. French government bonds also sold off as the yield on 10-year French government bonds increased 0.2% at the start of the week. Although they recovered slightly as the week progressed.

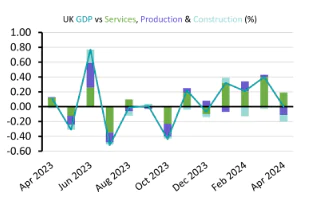

UK : Growth flat lines and employment cools

The UK’s economic growth from the first quarter evaporated in April as the size of the UK economy was unchanged. Growth in the services sector slowed but it was still enough to offset a drop in construction activity. The slowdown is noticeable after the relatively strong growth seen in the first quarter. There is more evidence that higher rates are having an effect on the UK’s jobs market. The unemployment rate continued rise as it ticked up again last month to stand at 4.4%. This is a marked increase from the rate of 4% in January. Average wages are still rising faster than inflation, but there are other signs of hiring slowing down as the number of job vacancies has continued to decline.

The lack of growth and worsening job market but the Bank of England is still expected to cut rates this year and the expected timing of rate cuts has helped UK government bonds rise without the volatility seen in US and European markets, and as helped the pound to appreciate against the dollar and the euro.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of

Private Office Asset Management and should not be construed as advice. This is not a financial promotion.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.

Yours sincerely,

Phil Simmonds