Market Update week ending 12 May 2023- BANK OF ENGLAND RAISES RATES IN FIGHT AGAINST INFLATION

![]()

BANK OF ENGLAND RAISES RATES IN FIGHT AGAINST INFLATION

Last week there was further evidence of the split emerging between the US Federal Reserve and central banks on this side of the Atlantic. The decline in US inflation takes the pressure off the Fed as it can argue that it should now be given time to see if its efforts have paid off. Over here the data is far from convincing. GDP growth remains weak, at just 0.1% for the first quarter. Unemployment is very low and wages are rising, but signs of weakness are emerging – particularly in employers’ preference for temporary staff over permanent hiring. As the Bank of England has conceded that inflation will remain higher for longer markets now expect several more hikes before it is ready to pause for reflection.

Elsewhere, big tech companies continue to hype the potential for artificial intelligence. However, the impact is already being felt in sectors like publishing, marketing and advertising as investors grow concerned about its impact. Businesses like Pearson and Relx have spent this week outlining the benefits they see in AI but there is likely significant disruption to other sectors as the potential for this technology is tested

![]()

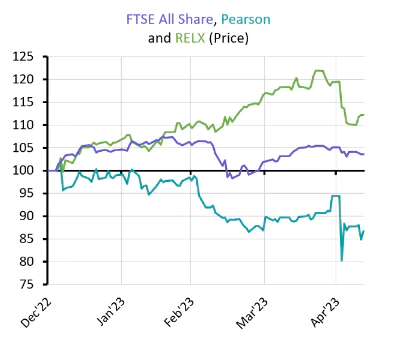

GLOBAL : EDUCATION STOCKS LOOK FOR THE POSITIVE IN AI

This week Google announced it has incorporated generative AI in a number of its products, including its online search tool, to improve results. This is the latest attempt by a big tech firm to demonstrate an ability to use natural language chat-based interfaces as a way of improving its service and highlight its importance for future growth. Microsoft recently added ChatGPT to its Bing search function and Meta also pointed to its use of AI to improve Facebook and other social media apps.

Meanwhile other firms have been trying to prove that AI is not a threat. Shares in US tutoring and revision service Chegg fell 40% after it warned that ChatGPT is already causing subscribers to fall. This dragged on the shares of other education service providers. This week Pearson delivered an update to highlight the potential benefits to its business and Relx was also scheduled to give an update on how AI will benefit its business. After a sharp fall last week, UK advertising and education providers have seen their share prices stabilise.

![]()

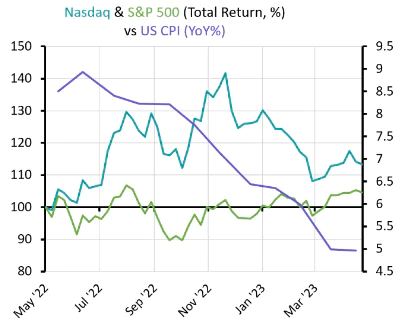

US : INFLATION FALLS BUT GOVERNMENT DEBT STAND OFF RATTLES BOND MARKET

US inflation slowed further as the headline Consumer Price Index fell from 5% to 4.9% in April. Core inflation also fell slightly to 5.5%. The significant drop in energy prices in the US mean energy is now deflationary, but the costs of housing and services continue to rise strongly. The relatively small increase in new jobs has also supported the view that the US central bank has reached the end of its rate hiking cycle. This helped boost US equity markets, with technology stocks seeing the biggest benefit.

The outlook for US government bonds has been complicated by concerns about the potential for a default. US government borrowing can only be increased by Congress and President Biden only has a short time to convince Republicans to back his spending plans. Some forecasts say the debt ceiling will be hit in early June and short-dated bonds have sold off against the possibility that no agreement will be reached.

![]()

US GOVERNMENT BORROWING / DEBT MOUNTAIN – SOME PERSPECTIVE

US national debt currently stands at around US$31.5 trillion, daily reporting from the Treasury shows. The US officially hit its debt ceiling of US$31.4 trillion on 19th January this year. Last year I wrote an article on US Independence day, 4th July 2022 examining their then debt mountain of US$27 trillion – which had itself had risen US$9.3 trillion in the previous 13 years since the financial crisis, though supposed ‘boom’ times for the economy. The latest figures show an increase of a further US$5.5 trillion (US$4,500,000,000,000) from July 2022 to January 2023 – in just 6 months, – since which we have seen Silicon Valley Bank goes bust with US$210 billion of assets and the Swiss banking giant Credit Suisse also effectively going to the wall, – with further US provincial banks also hitting trouble more recently.

Me and my team were recently attending a local continuing professional development event run by a household name global investment house, and the first speech was by one of their senior economists discussing the huge losses made last year across almost all bond markets, defending their own significant losses as better than the average across the whole sector, equities too, – and then providing graphs dating back to Black Monday 19th October 1987 when 30%+ of market valuations was wiped off in a single day, – and then showing the inflation numbers, interest rate figures and then recovery’s following such events. The idea is for the financial advisers attending the event to buy in to their ethos and skills in managing client funds and to convince the audience that they had been through it all and seen it all, and that they were just in the right side of better than average.

The one question that was put to the speaker in the room was asked by myself, and it related to national debt across the developed nations and the impact it has on such recoveries. My question was why, having out together all of the presentation with a plethora of supporting graphs dating back to the 1987 crash, why there was not a single graph on the levels of national debt of, say the US, during and post each period, – because as I suggested, that really was the elephant in the room that was simply not discussed or taken into consideration at all. The answer from the economist presenting the data was that, firstly it was an excellent question, but the answer was certainly not an answer worthy of such. The answer was that yes, debt had spiralled, but that as long as there were buyers of that debt then there wasn’t a problem!! The difficulty in furthering such discussions in a public forum is firstly there is a time pressure, second, they have their scripts, and this clearly wasn’t an expected or anticipated question, thirdly there is usually one or 2 sceptics in the audience and they are often seen as simply being negative, and thirdly, they were supplying a nice lunch! I did put one more thought forward, which was that in my opinion of course it matters greatly, – because back in 1987 the US national debt was only US$2.35 trillion compared to US$31.5 trillion today – and so the interest payments to service the debt make up a relatively very significant of the US economy’s output which means less investment, higher taxes, a government that needs inflation in the system to erode the real value of their debt (even though they might pretend otherwise – but think it through, – if inflation is running at 10% then the real value of US$31.5 trliion reduces in real value terms by US$3.15 trillion in a single year – in the case of the US this is a reduction of more than the entire US national debt back in 1987 which stood then at US$2.35 trillion and was considered high at that point in time).

With a rising debt mountain this leads to ever increasing borrowing requirements to service the debt and essentially the fundamental economics become skewed, – just like if a household had debt that it will never be able to afford to clear, there comes a point where you are simply robbing Peter to pay Paul until it all comes crashing down. This will impact both short & long term interest rates, especially the major economies printing vast amounts of money (Quantitative Easing) to get through the 2008/2009 financial crisis and then the Covid pandemic which by itself will of course add to inflationary pressures and so the wheel of increasing debt keeps turning. We are now at the point where the developed world can only hope to service it’s debt, but they will never be able to clear it. And yet the large household name investment institutions ignore the impact of all this debt. We however did not, – which is why we always have one eye on keeping volatility as low as possible across all of the various client risk profiles.

I would just remind our readers of our concerns about world debt and its potential impact by considering for a moment the vast scale of the debt. Most people cannot comprehend what a trillion even looks like. In space the distances are in trillions of miles and they are so huge that astrophysicists and cosmologists measure distances, not in trillions of miles, but in “light years”.

![]()

Allow me introduce you to Alpha Centauri on the left, one sun in the triple star system located 25 trillion miles from our earth and sun, the nearest star in its system to our solar system being “Proxima Centauri”. Because of the vast distances across space, cosmologists do not refer to the distance in miles because 25 trillion miles is difficult to comprehend. Instead, they use the term light years – 1 light year being the amount of distance that light travels in one year. So, with light travelling at 187,000 miles per second, which is approximately 1 million miles every 5 seconds, it takes light 4.3 light years to travel between our solar system and Alpha Centauri. To further put that into perspective, it would take the Saturn V Rocket, the most powerful rocket ever built by man, 100,000 (one hundred thousand) years to travel between our solar system and Alpha Centauri at full pelt with no gravitational or wind resistance in the vacuum of space.

The key point, and this to a lesser but comparable degree is true of all of the world’s “richest” nations – the US debt mountain is so huge that as light travels between our mother Earth and Alpha Centauri at 187,000 miles per second, – if it had just the US Federal debt in tow, – it could drop a US1Dollar note of its debt each and every single mile of its journey of around four and a half years at 1Million miles every 5 seconds, and still have enough USDollars of debt in tow to travel back to earth dropping a single US$1 Dollar bill every mile for 8 months of its return journey at 187,000 miles per second. The enormity of the debt problem is not just confined to the US but also Japan, the EU, the UK and other nations, whose own debt mountains have also risen to previously unimaginable numbers, – but topical again here as the US once again reaches its increased debt ceiling, where Congress and the Senate will need to agree to raise it, once again, in order for it to be able to continue it’s instruments of basic government.

Twice during the Barack Obama Presidency the US government ground to a halt, whilst seeking an increase in the debt ceiling by Congress and the Senate. Far from the problem going away, the debt mountain continues to grow, with global investment institutions barely acknowledging it’s existence let alone the problems that come with it, which includes significant banking failures as noted above, – which were caused, and acknowledge as being caused by the knock on effects of the last 18 months of interest rate rises, which were allegedly necessary to fight inflation (despite inflation being caused almost exclusively by the “imported inflation” of energy prices and rising food prices – which actually had little to do with consumer spending), – and those interest rate hikes 100% predictably saw bond yields rise sharply as the underlying values of the vast amount of bonds held by these banks plummet which in turn saw their balance sheets tumble to the point where their assets were no longer enough to support their business model. Make no mistake about it, the level of government debt had a large part to play in that because it directly affects their monetary policies with rising taxes across a smaller pool of tax payers, inflation coming into the system spurred on by previous QE – the governmental (central banks) decisions to print more money to buy back its debt because they cannot complete with the risk free rate market to issue new debt to cover the cost of supporting their respective economies following the financial crisis and covid (to name but 2 reasons) and the resultant interest rate rises to fight the inflation they have actually had a major hand in causing, which sends bond prices plummeting, asset prices following suit and resulting bank failures because they are holding too many bonds which crashed in value which in turn effectively killed their balance sheets. But yet, global investment houses are virtually ignoring the developed nations debt, merely stating that as long as there are buyers of the debt, there is not really a problem!?

UK : BANK OF ENGLAND HIKES RATE BY 0.25% TO 4.50%

The Bank of England increased interest rates by 0.25%. The increase was widely expected but it indicated that further hikes may be needed, as it said inflation will remain sticky and the economy is expected to avoid recession. The bank previously tipped inflation to fall to 3.9% by the end of 2023 but it now expects inflation to be 5.1% and does not expect it to return to the 2% target until 2025. The better outlook for global growth and lower energy prices have improved the bank’s outlook for the UK. However, a stronger economy gives the bank more leeway to increase rates to help bring inflation down and markets now expect base rate to rise to around 5% this year.

The UK jobs market remains relatively robust, although there are signs it is starting to cool. The Recruitment and Employment Federation reports that hiring of permanent staff fell for the seventh consecutive month. Recruiter Reed said average salaries for new employees are around 10% up from last year, but it expects this to fall quickly in the second half of the year. A barrier to the jobs market of course is the ever more burgeoning employment law, which we would argue does need to be scaled back.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.

Yours sincerely,

Phil Simmonds

Philip A. Simmonds LL.B(Hons), MBA, FPFS, Chartered MCSI

Chief Executive Officer | Solicitor-Advocate (non-practising) Chartered Wealth Manager | Chartered Financial Planner