MARKET UPDATE – Week ending 1 March 2024 USA – CORE INFLATION FIGURES RESUME DOWNWARDS TREND

USA – CORE INFLATION FIGURES RESUME DOWNWARDS TREND

This week investors breathed a sigh of relief as US core inflation resumed its downward trend. The Core Personal Consumption Expenditure Price Index is a significant measures of US inflation as it is closely watched by the Federal Reserve. After appearing stubbornly high at the previous two readings, the small move down this month has been welcomed by those concerned that central bank rate cuts were in danger of being delayed. We’ve also seen headline CPI inflation in Europe decline due to disinflation in France and Germany.

However, there are signs that controlling inflation fully may be difficult. US Core PCE is down over one year, but the monthly reading picked up. Meanwhile, goods prices are falling but services inflation is still rising strongly on both sides of the Atlantic. In the UK, for example, Halfords is feeling the effect of less spending on goods while IAG is the latest airline to cash-in on the post-Covid travel boom. As pointed out by Bank of England member Catherine Mann, a lot of inflationary spending is coming from wealthy consumers who are not affected by higher borrowing costs.

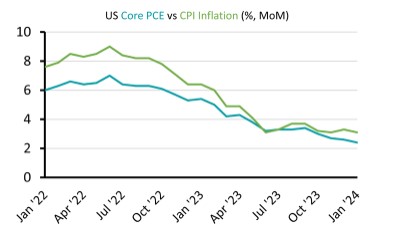

![]() US : MARKETS REASSURED AS CORE INFLATION FALLS

US : MARKETS REASSURED AS CORE INFLATION FALLS

US and UK government bonds rallied after US core inflation fell to 2.4% for the year to February. Core consumer inflation is a key measure for the US Federal Reserve as it considers the path for US interest rates. There were fears that core inflation was proving resilient as it remained unchanged between November and December but the return of disinflation reassured bond markets that the Fed remains on track to cut interest rates. Other measures of the US economy show some weakness. Durable goods orders declined in February as companies reduce investment and the US housing market remains subdued.

The return of disinflation also helped boost US equities, despite attempts from Federal Reserve members to calm hopes of an early rate cut. Several members of the Federal Open Markets Committee warned that the bank would be driven by the economic data available and that there may be fewer rate cuts than markets expect.

UK : POOR EARNINGS DRAG ON MARKET

UK : POOR EARNINGS DRAG ON MARKET

UK equities were dragged down as several stocks tumbled after issuing profits warnings. Shares in wealth manager St James’s Place fell 30% after it cut its dividend and put aside £460m to pay for potential fee refunds. Halfords shares declined around 25% after weak consumer sentiment and wet weather effected sales. Reckitt Benckiser also fell significantly after sales contracted. The troubles are mainly down to company-specific problems, but the impact of weak consumer spending on Halfords and Reckitt Benckiser raises questions about the resilience of consumer facing businesses.

Several large US tech companies also reported sales below expectations. Cloud computing firm Snowflake and software company Salesforce fell as both said sales growth has slowed and warned of a tougher conditions ahead. Google-owner Alphabet also fell after it was sued by 30 European media organisations who accuse it of artificially depressing advertising revenues. However, US stocks recovered as core inflation declined as expected.

LONDON STOCK EXCHANGE : LSE LOOKS TO BRIGHTER FUTURE AS SHEIN EYES LONDON IPO

LONDON STOCK EXCHANGE : LSE LOOKS TO BRIGHTER FUTURE AS SHEIN EYES LONDON IPO

The London Stock Exchange (LSE) expects to see more companies list in the UK as online retailer Shein said it is considering switching its planned IPO from New York. LSE Group said revenues from UK equity trading declined last year but there is a good pipeline of new listings in 2024. Shein faces political obstacles to listing in the US and a switch to London would be boost after the UK recently missed out on several high-profile IPOs. Shein is one of the world’s largest clothes retailers with revenues around $22bn. An IPO could value it between $5bn and $10bn.

Relatively low valuations in the UK are a major reason for companies choosing US listings instead. Sterling weakness has also made UK companies attractive to overseas buyers. This week Currys turned down an improved offer from Elliott Management as management says the offer undervalues the business. In addition, Direct Line received an approach from Belgian insurer Ageas and Wincanton received a bid from US rival GXO.

Please note that t he opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset Management and should not be construed as advice.

he opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset Management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.

Yours sincerely,

Phil Simmonds

Philip A. Simmonds MBA, LL.B(Hons), FPFS, Chartered MCSI

Chartered Wealth Manager | Chartered Financial Planner

Solicitor-Advocate (company in-house solicitor)

E : phil.simmonds@private-office.co.uk

phil.simmonds@private-office.law (for legal matters)

This document has been prepared for general information only and is not guaranteed to be complete or accurate. It does not contain

all of the information which an investor may require in order to make an investment decision. If you are unsure whether this

is a suitable investment you should speak to your financial adviser. You may get back less than you originally invested.

Private Office Asset Management is authorised and regulated by the Financial Conduct Authority