Market update 16 June 2023 – US FEDERAL RESERVE & EUROPEAN CENTRAL BANK STICK TO THE SCRIPT

![]()

US FEDERAL RESERVE & EUROPEAN CENTRAL BANK STICK TO THE SCRIPT

Last week’s central bank interest rate decisions came in as expected. The Federal Reserve left rates unchanged – the first time it has opted not to hike since March 2022 – while the European Central Bank increased rates by 0.25%. The ECB maintained its aggressive attitude to tackling inflation, effectively promising another hike next month, but the Fed was a bit more aggressive than expected. US inflation is heading in the right direction but progress is slow and the jobs market remains robust. Fed members indicated that two more hikes are likely this year and Fed chair Jerome Powell signalled that rates will need to remain elevated to avoid a stop/start approach to tackling inflation.

Next week brings UK inflation data and the Bank of England’s interest rate decision. Strong employment and GDP data have convinced investors that the UK will also be more aggressive and UK gilts were dragged down again. As ever, the higher rates go, the greater the chances that something in the economy breaks. Rising mortgage costs and soaring insolvencies offer a reminder that we may not be too far from that point.

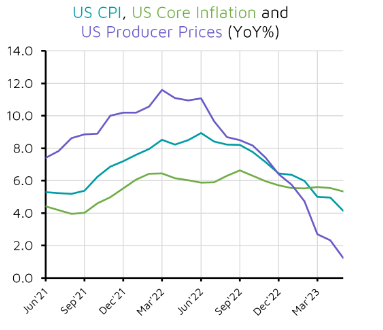

![]() US : FEDERAL RESERVE HITS THE BRAKES (FOR NOW AT LEAST)

US : FEDERAL RESERVE HITS THE BRAKES (FOR NOW AT LEAST)

The Federal Reserve opted not increase interest rates at its monthly meeting following confirmation that inflation is falling in the US. Headline inflation continues to drop steadily as the annual rate for the Consumer Price Index fell from 4.9% to 4% helped by falling energy prices. Core inflation (excluding more volatile energy and food costs) also slowed but the decline was more modest as the annual rate dropped from 5.5% to 5.3%. Costs for producers also eased as the Producer Price Index dropped from an annual rate of 2.3% to 1.1%.

Falling inflation meant the Federal Reserve left interest rates unchanged at 5.25%. This is the first time the Fed hasn’t increased rates since it began the current hiking cycle in March 2022. However, the Fed said that further rate hikes are likely to be necessary later this year. US equities have continued their recent rise but US government bonds declined slightly this week. As expected, the European Central Bank raised interest rates by 0.25% to 3.5%.

UK : ECONOMIC DATA SIGNALS FURTHER RATE RISES

UK : ECONOMIC DATA SIGNALS FURTHER RATE RISES

UK government bonds fell and yields rose sharply as positive economic data increased the chances of further rate hikes from the Bank of England. Employment increased in the three months to April. The number of people unemployed increased very slightly but the number of those classed as inactive fell. Average wages continued to rise faster than the long-term average as they increased by 7.2%. The number of job vacancies fell slightly but remains above 1 million. Economic growth also ticked up slightly in April as more consumer spending offset a slight decline in manufacturing.

Better economic data means the Bank of England is expected to raise interest rates more aggressively to bring inflation under control and markets now forecast rates to peak well above 5%. This has driven up the cost of mortgage borrowing and has pushed yields on UK gilts up to levels seen during last autumn’s disastrous mini-Budget. Sterling has continued its recent rise against the dollar.

![]() GLOBAL : INITIAL PUBLIC OFFERINGS (LISTINGS) FALL SINCE PANDEMIC

GLOBAL : INITIAL PUBLIC OFFERINGS (LISTINGS) FALL SINCE PANDEMIC

Turkish soda ash maker WE Soda has cancelled its planned listing in the UK after blaming extremely cautious investors for a lack of interest. The initial valuation of £6bn would have made it one the biggest UK listings in recent years. WE Soda said investor caution meant it felt the initial public offering would fall short of its own valuation.

The number of companies choosing to list in London has fallen dramatically in recent years. Chip designer Arm was previously listed in the UK but has chosen New York for its return to public markets later this year, and building materials group CRH last week confirmed its switch from London to New York. Recent reports have blamed the decline on higher taxes, excessive regulation and a lack of investor interest. However, there are signs that UK listings are picking up. There were six new listings on the main market in London last month, and CAB Payments confirmed its plans for a London listing which could value the firm somewhere between £800m and £1bn.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.