END OF US BUDGET SQUABBLES IN SIGHT – Market Update Monday 22 May 2023

![]()

END OF US BUDGET SQUABBLES IN SIGHT

An agreement to raise the debt ceiling and avoid the US defaulting on its debt could be struck on Capitol Hill this weekend. Markets will be pleased by the end of the recent brinkmanship, in which Republicans have used their majority in the House of Representatives as leverage over President Biden and his agenda.

The Bank of England’s top economist apologised for saying that people must “accept they are poorer”. Huw Pill said Britons needed to stop asking for pay rises to keep up with soaring prices because this risked keeping inflation higher for longer. Mr Pill said he sorry for using “inflammatory” language and said he should have used “somewhat different words”. However, his boss, the central banks Governor Andrew Bailey, conceded that some of the UK inflation now coming through was due to secondary factors, such as pay rises – and the Bank of England was dealing with a wage-price spiral. He is therefore keeping the door open for further interest rate rises later this year.

Inflation may be proving to be a stubborn issue in the West, but data from Argentina was particularly sobering. Inflation hit 109% in April, prompting the Central Bank of Argentina to raise its key interest rate by 6 percentage points to a staggering 97%. Only Venezuela and Zimbabwe are currently experiencing higher price issues, according to the International Monetary Fund.

All of that said, this week has seen some optimism creeping into equity markets, although bond investors continue to take a gloomy view. The potential for default in the US has pushed yields on the shortest Treasury Bills to their highest level since the financial crisis, while the yields on longer-dated bonds show investors expect the Federal Reserve to cut rates as the economy deteriorates.

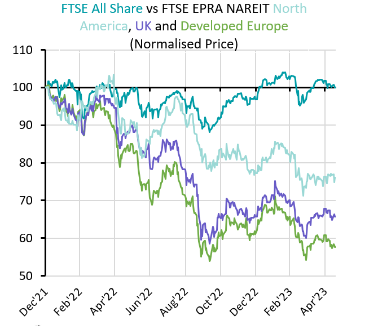

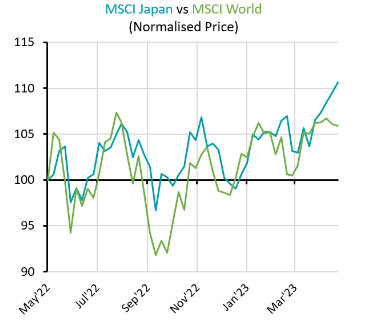

A disconnect between equities and bonds can been seen in other markets too. Japanese equities have been rising recently, but the outlook for bonds remain more cautious. Meanwhile, UK equities have risen strongly since the dip in mid-March and the FTSE-100 is one of the better performing indices this year. Again, bonds have taken a leg down as the Bank of England signals it may continue hiking rates. Consensus often contributes to complacency in financial markets, and widespread agreement raises the possibility of a major shock, but both markets cannot be correct.

UK INTEREST RATES : BANK OF ENGLAND QUOTES WAGE SPIRAL

UK INTEREST RATES : BANK OF ENGLAND QUOTES WAGE SPIRAL

As noted above, The Bank of England’s governor, Andrew Bailey, warned the UK is experiencing secondary inflation effects as higher prices caused by supply chain disruption and high energy costs have given way to price increases caused by employers needing to cover higher wage demands. However, the latest UK employment data shows the jobs market remains robust. The employment rate has ticked up slightly as some people who chose to stop working during the Covid pandemic return to employment and wages continue to rise at a much faster rate than in recent years, as average private sector wages increased by 7%.

Last week, the Bank of England also raised its forecast for inflation. It now expects inflation to remain above 5% this year and not to return to the target 2% until 2025. Andrew Bailey’s comments that the Bank of England would raise rates as far as necessary to get inflation back to target contributed to a decline in gilts as the yield on 10-year UK government bonds rose to the highest level this year, – meaning of course that the underlying value of those gilts fell accordingly.

UK PROPERTY SECTOR : OFFICE VALUES SERIOUSLY DAMAGED

Some of the UK’s biggest commercial landlords have been setting out the damage caused by soaring interest rates and the growth in the working from home culture. Land Securities and British Land said their central London offices have fallen in value by 8% and 12% respectively over the past year as higher rates and the rise of working from home has combined to dent valuations and reduce demand. Last month, Segro reported the continued decline in the value of its industrial properties, although it said a shortage of supply is supporting rental income.

However, Land Securities and British Land say demand for prime central London offices remains strong and reported rising rental income. With the Bank of England expected to stop hiking interest rates before the end of the year, British Land chief executive Simon Carter actually expects central London property values to stop falling. Commercial landlords are also hoping to see demand for office space continue to rise as employers encourage people to spend less time working from home, although older buildings with poor energy efficiency are likely to remain unpopular.

JAPAN : EQUITIES GAIN AS ECONOMY GROWS

JAPAN : EQUITIES GAIN AS ECONOMY GROWS

Japanese equities have risen to levels not seen since the early 1990s as the drop in the yen and improving corporate governance attract investors. The broad Topix index and the larger companies Nikkei 225 index have risen strongly, with the Topix up around 14% in the last 12 months. The effect of currency exchange means UK investors have gained around 7.5%, but this is second only to Europe over the last year.

Japan is also experiencing stronger economic growth. GDP rose by 0.4% in the first quarter of the year, and annual growth is now around 1.5%. This compares to the forecast of -0.2% for the UK. The Japanese economy has benefited from stronger consumer spending following the removal of Covid restrictions. Japan does face some headwinds as the government is expected to begin reversing the huge fiscal stimulus programme and decades of ultra-low interest rates, and this could see the yen appreciate. It’s strong trade links with China mean exports could weaken if Chinese growth falters.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset management and should not be construed as advice.