DEVELOPED ECONOMIES CONTINUE TO STRUGGLE WITH INFLATION – Market Update week ending 9 June 2023

![]()

DEVELOPED ECONOMIES CONTINUE TO STRUGGLE WITH INFLATION

This week we saw continued signs of divergence across the global economy as various regions battle inflation. The three most likely outcomes for inflation are; receding without a recession – the fabled soft-landing; inflation falling on the back of an economic contraction – a hard landing; or, inflation staying higher for longer – no sign of a landing yet! It looks like all three are taking hold depending on the region. In the UK inflation is coming down slower than hoped for, while in Europe news that inflation is falling rapidly but the region has entered a technical recession suggests a hard landing could be on the cards. Meanwhile, in the US robust jobs numbers mean it still has a chance of pulling off a soft landing.

Elsewhere, it looks like China has got off to a false start with its own delayed Covid recovery. After it ended its severe Zero-Covid lockdown policy, many expected a surge in economic growth to follow. There was an initial bounce back but recent data suggests that the growth is stalling and that the result may be deflation, a major divergence

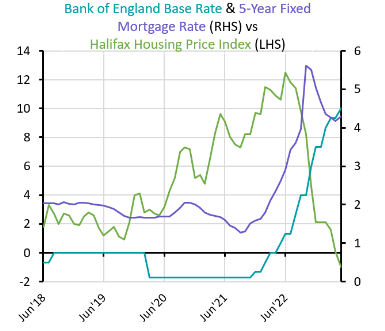

UK : HOUSE PRICES DECLINE AFTER A DECADE OF GROWTH

UK : HOUSE PRICES DECLINE AFTER A DECADE OF GROWTH

Rising mortgage costs and squeezed affordability have been blamed for the first annual decline in house prices since 2012. The Halifax house price index is 1% below the level this time last year as average prices have fallen steeply since their peak last summer. Mortgage rates have doubled in the last 12 months while high inflation has hit affordability as borrowing rates are rising as lenders expect the Bank of England to hike rates again. The Royal Institution of Chartered Surveyors says the outlook has improved but sentiment remains very low compared to the long-term average.

Construction output in the UK remains positive. However, an increase in commercial and industrial construction is offset by a significant decline in housing. House builder Crest Nicholson reported that profits fell by 60% and completion of new projects fell by 20% in the six months to April, as it warned that rising interest rates will continue to undermine buyers’ confidence and depress demand.

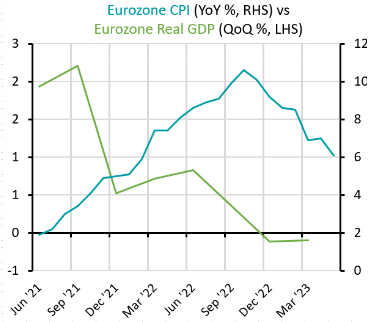

EUROPE : EUROZONE SLIPS INTO RECESSION

EUROPE : EUROZONE SLIPS INTO RECESSION

The Eurozone is already in recession according to the latest data from the European Union. The last two quarters of GDP growth have been revised to reflect slightly worse data from Germany. The Netherlands and Ireland also saw their economies contract slightly. The previous figure of 0% GDP growth for the first quarter of this year has been restated as a decline of -0.1%. Growth for Q4 2022 of 0.1% has also been revised down to a -0.1% decline meaning the Eurozone is already in a mild technical recession.

The European Central Bank remains committed to raising interest rates and the slight deterioration in economic growth is unlikely to change its outlook. However, government bonds have fallen again after the Reserve Bank of Australia and the Bank of Canada unexpectedly increased rates this week. Their more aggressive approach has caused markets to consider whether the Federal Reserve will hike again at next week’s interest rate meeting, rather than keep rates on hold as previously expected.

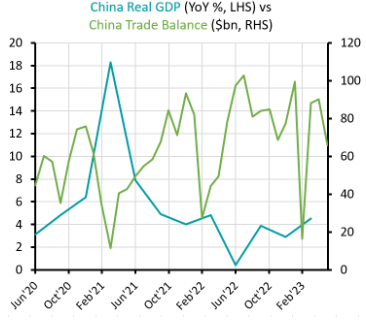

CHINA : ECONOMIC GROWTH STALLS AS TRADE FALLS

CHINA : ECONOMIC GROWTH STALLS AS TRADE FALLS

Chinese trade fell sharply last month in the latest sign that the country’s return to economic growth is not running smoothly. Exports were expected to slow but remain positive after the 8.5% monthly increase recorded in April. However, exports fell by 7.5% instead. Imports also declined, although at a slower pace. Instead of the slight increase expected, the balance of trade dropped from $90bn to $65bn in May.

Other economic data show China’s economy struggling to regain its pre-Covid momentum. Although services output, measured by S&P Global Purchasing Managers’ Indices, continues to grow, official data shows manufacturing output contracting. Despite weaker output from China, the OECD and the World Bank have both slightly upgraded their forecasts for economic growth this year and the OECD said it expects China to exceed its official growth target of 5% for 2023. China’s six biggest state-run banks all cut their deposit rates this week in an effort to stimulate spending in the latest effort to kick-start its economy.

Please note that the opinions expressed in this newsletter are those of the author, and they do not purport to reflect the opinions or views of Private Office Asset management and should not be construed as advice.

If you enjoy reading this weekly update, please feel free to share it with your friends and / or family who may also find the contents of interest, and do not hesitate to contact us if you need any help, information or advice yourself about any of the areas covered this week.